By MajorMedicalInsurance.com Editorial Team

Published on · Updated on

Cancer survivorship often means more than one doctor visit a year. It can involve follow-up oncology appointments, prescription drugs, imaging, lab work, preventive screenings, mental health support, and protection against a possible recurrence or a new diagnosis. That is why major medical insurance matters so much for cancer survivors: the goal is not just to have coverage, but to have coverage that still works when care becomes expensive and ongoing.

Quick Answer

For most cancer survivors, the most important insurance protections are coverage for pre-existing conditions, access to comprehensive medical benefits, strong prescription drug coverage, in-network access to the doctors and facilities you actually use, and a manageable out-of-pocket maximum. The best plan is usually not the one with the lowest premium. It is the one that gives you the best balance of provider access, drug coverage, and financial protection.

Why Major Medical Coverage Matters After Cancer

The Affordable Care Act changed the insurance landscape for cancer survivors. Marketplace plans must cover treatment for pre-existing conditions, and insurers cannot reject you, charge you more, or refuse to pay for essential health benefits because of a condition you had before coverage started. For a more detailed breakdown, see pre-existing conditions and major medical insurance.[1] That is one of the biggest reasons major medical coverage is different from temporary or limited-benefit products.

Marketplace plans must also cover the 10 essential health benefit categories. These include hospitalization, outpatient care, emergency services, prescription drugs, laboratory services, mental health and substance use treatment, rehabilitative services, and preventive care.[2] For survivors, that broader structure matters because cancer-related costs are rarely limited to one type of service.

For a broader foundation, you can also compare major medical health insurance and what major medical insurance covers.

The Main Coverage Paths Cancer Survivors Usually Compare

Marketplace or Other Individual Coverage

If you are buying your own insurance, ACA-compliant Marketplace coverage is usually the most important place to start because of the pre-existing-condition protections and essential health benefits described above.[1][2] This is often the most relevant path for people between jobs, self-employed survivors, or those who do not have access to job-based coverage.

Employer Coverage and COBRA

If you already have good job-based coverage and then lose your job or work hours, COBRA may let you keep that same group health coverage temporarily. The U.S. Department of Labor says COBRA generally lasts 18 to 36 months depending on the qualifying event, but the plan may require you to pay the full premium plus up to a 2% administrative fee.[3]

Why COBRA can still matter

For a survivor who is already in active follow-up care, COBRA may help preserve continuity with the same doctors, facilities, and drug coverage. The tradeoff is cost, because employer contributions often end and the full premium shifts to you.[3]

Medicare

Medicare can be relevant if you are 65 or older or qualify through disability. Medicare covers many medically necessary cancer-related services, including chemotherapy and radiation treatment in the appropriate outpatient or inpatient settings.[4] If that is your situation, it often makes more sense to compare Medicare separately instead of trying to force every decision into the individual-market framework.

What Cancer Survivors Should Check Before Choosing a Plan

For cancer survivors, plan documents are not optional. They are often the difference between a plan that looks good on paper and one that actually works in practice. Before enrolling, it is worth checking:

Use this checklist before you enroll

- Are your oncologists, surgeons, hospitals, and imaging centers in-network?

- Are your current drugs on the formulary, and on what tier?

- What is the deductible?

- What is the annual out-of-pocket maximum?

- How does the plan handle specialist visits, imaging, infusion, and outpatient hospital care?

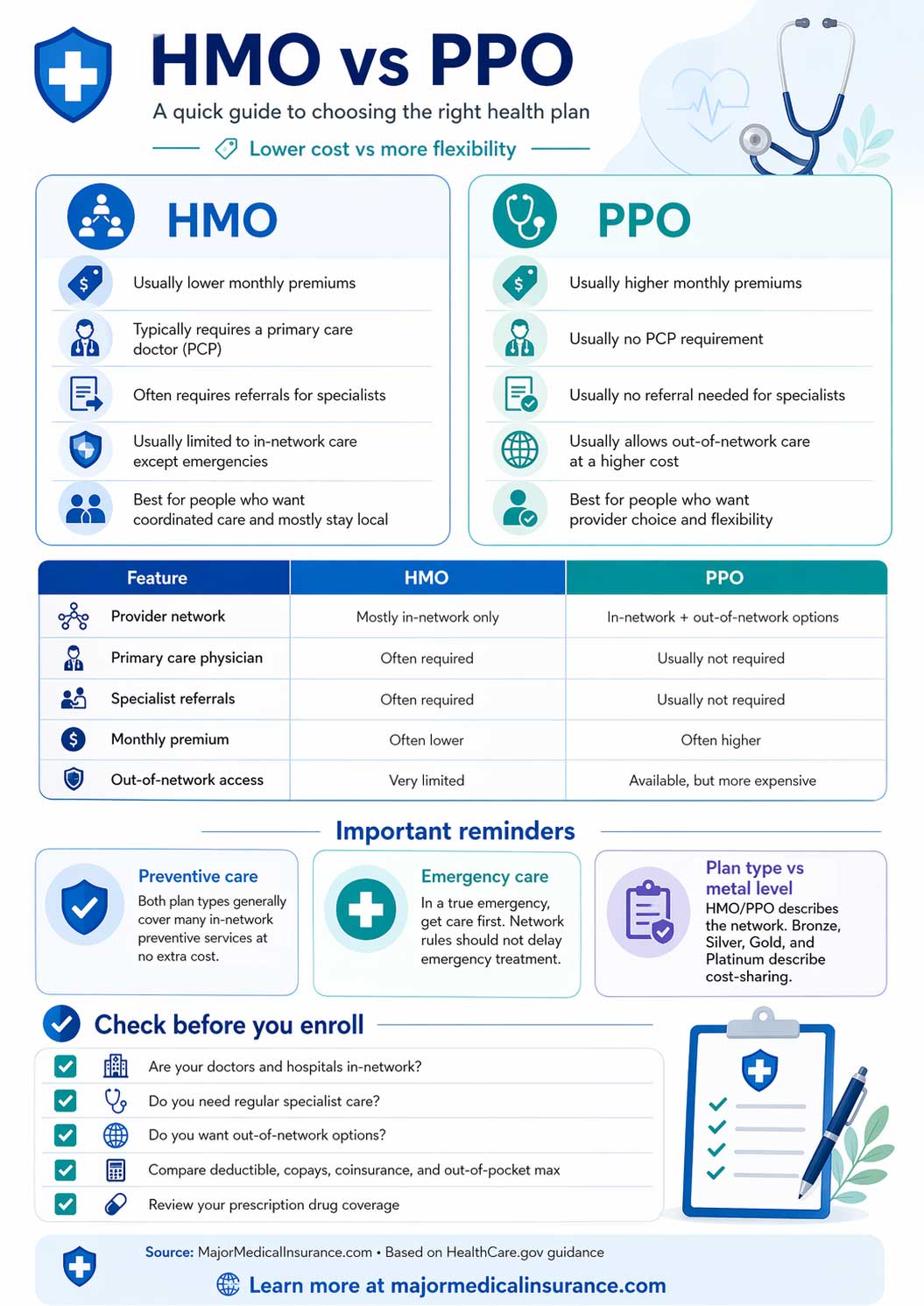

- Do you want a lower-cost HMO or a broader-access PPO?

If you are still comparing network styles, medical plans HMO vs PPO are a useful next read.

Cost Protection Still Matters After Treatment

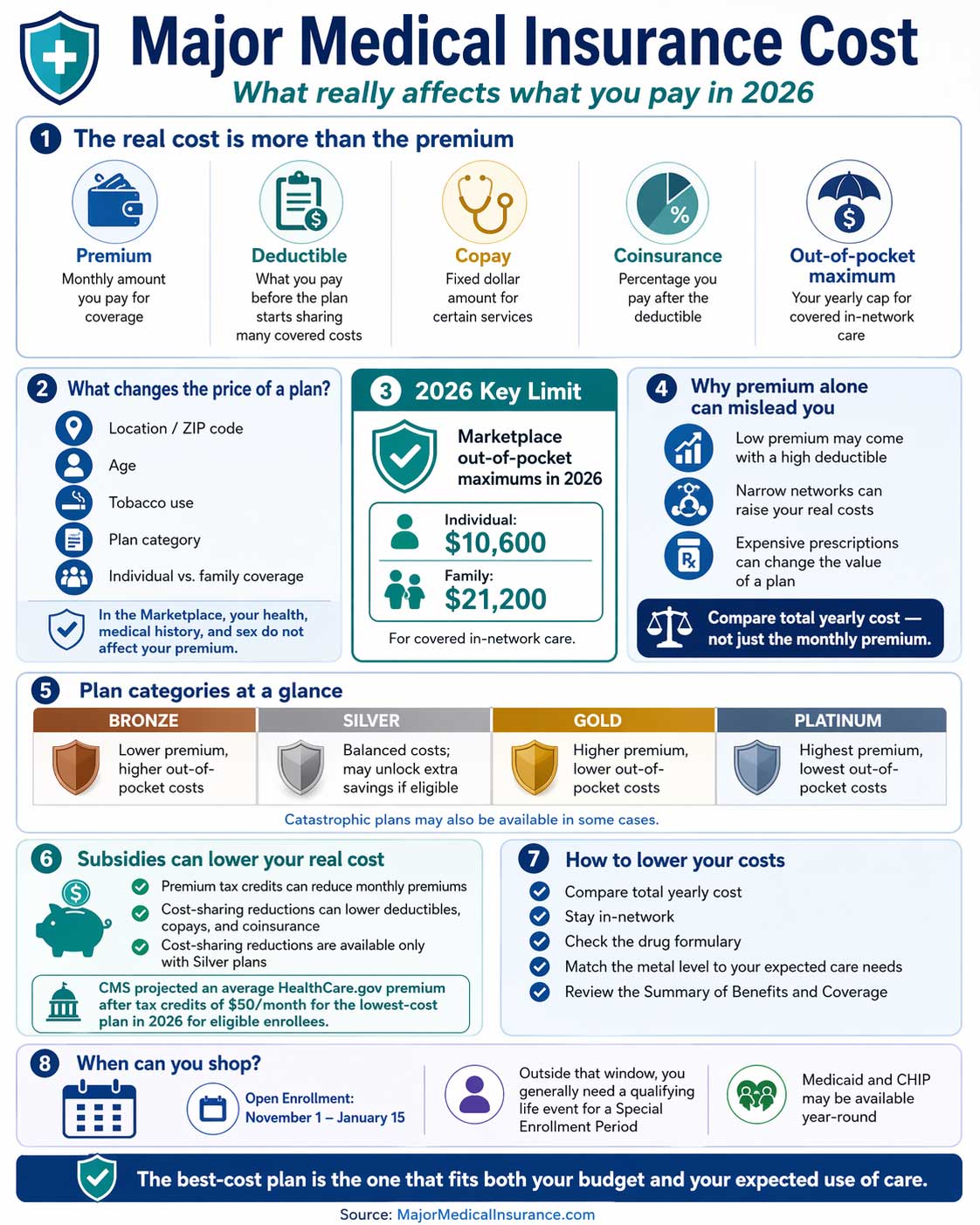

Major medical coverage is not just about access. It is about cost exposure. For many survivors, the right question is not “Will this plan pay for something?” but “How much could I still owe in a heavy-care year?” That is why deductible, coinsurance, and especially the annual out-of-pocket maximum matter so much.

HealthCare.gov says the out-of-pocket limit applies to covered in-network care. This is one of the most important protections in major medical coverage because it gives you a ceiling on what you may have to spend in a plan year for covered in-network services.[5]

Bottom Line

For cancer survivors, major medical insurance should be judged by what it does after the diagnosis, not just by the premium. The strongest plans usually combine pre-existing-condition protection, broad medical benefits, strong prescription coverage, survivorship-friendly provider access, and a manageable out-of-pocket ceiling.

References

-

HealthCare.gov, Marketplace health plans cover pre-existing conditions.

https://www.healthcare.gov/coverage/pre-existing-conditions/

↩ -

HealthCare.gov, What Marketplace health insurance plans cover.

https://www.healthcare.gov/coverage/what-marketplace-plans-cover/

↩ -

U.S. Department of Labor, COBRA Continuation Coverage.

https://www.dol.gov/agencies/ebsa/laws-and-regulations/laws/cobra

↩ -

Medicare.gov, Medicare Coverage of Cancer Treatment Services.

https://www.medicare.gov/publications/11931-medicare-coverage-of-cancer-treatment-services.pdf

↩ -

HealthCare.gov, Out-of-pocket maximum/limit.

https://www.healthcare.gov/glossary/out-of-pocket-maximum-limit/

↩