By MajorMedicalInsurance.com Editorial Team

Published on · Updated on

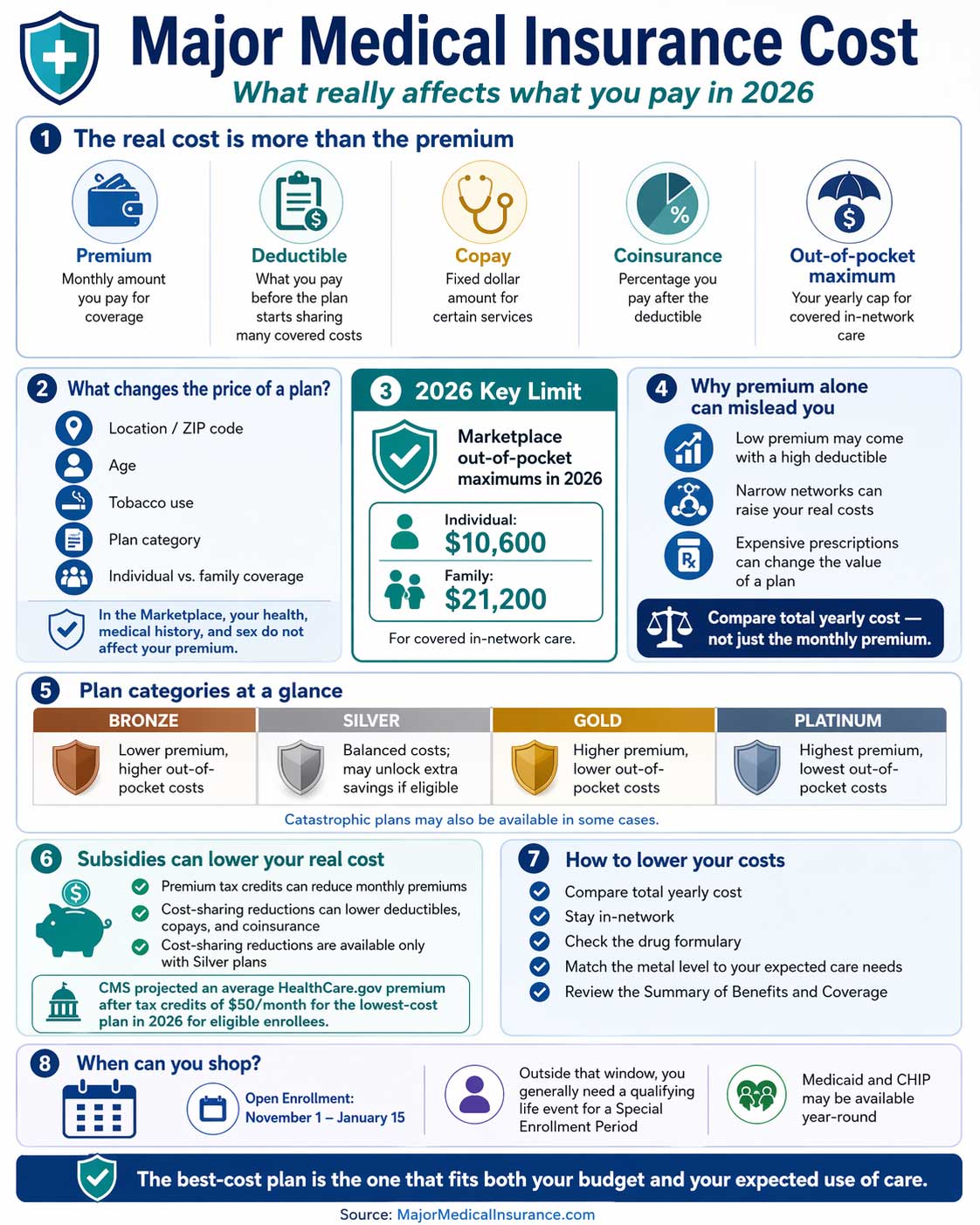

Major medical insurance cost is not just one number. The real cost of coverage includes your monthly premium, deductible, copays, coinsurance, and the most you could spend in a bad medical year. That is why a plan with a lower premium is not always the cheaper plan overall.

Quick Answer

The cost of major medical insurance depends on where you live, your age, whether you use tobacco, the plan category you choose, and how many people are covered. A smart comparison looks at total yearly cost, not just the monthly premium. For 2026, the out-of-pocket limit for a Marketplace plan cannot exceed $10,600 for an individual or $21,200 for a family for covered in-network care.[1][2]

What Makes Up the Cost of Major Medical Insurance?

Your total cost for health care is usually a mix of premium, deductible, copayments, coinsurance, and other out-of-pocket costs. That means a quote should never be judged on premium alone.[1] If you want a broader overview first, see major medical health insurance and what major medical insurance covers.

What Changes the Price of a Plan?

Marketplace premiums are not random. Five factors can affect a plan’s monthly premium: your location, age, tobacco use, plan category, and whether the plan covers dependents. Your health, medical history, and sex cannot affect your premium in the Marketplace.[2]

The biggest pricing drivers

- ZIP code and rating area

- Age

- Tobacco use

- Whether you choose Bronze, Silver, Gold, Platinum, or Catastrophic

- Whether you are buying coverage for yourself only or for a family

That is one reason national “average premium” claims can be misleading. A price that sounds low in one area may be irrelevant somewhere else, and two people in different age brackets may see very different premiums even for the same plan structure.

Why Premium Alone Can Mislead You

Shoppers should look at total costs, not just the monthly premium. A plan with a low premium can still end up costing more if the deductible is high, the network is narrow, or your prescriptions fall into expensive tiers.[1][5]

A simple way to think about cost

A low premium is good only if the rest of the plan still fits your real life. If you use specialists, expensive prescriptions, frequent labs, or ongoing treatment, a higher-premium plan may still be the better value because it lowers what you pay when you actually need care.

How the Deductible Affects Your Real Cost

Your deductible is the amount you generally pay for covered services before the plan starts sharing more of the cost. In practical terms, a higher deductible usually lowers the monthly premium, but it also means you may have to pay more out of pocket before the plan becomes more helpful.[1]

That tradeoff matters most when you actually expect to use care. Someone who mainly wants protection for major events may accept a higher deductible to keep premiums lower. Someone with regular specialist visits, imaging, or ongoing treatment may prefer a lower deductible even if the premium is higher, because the plan starts sharing costs sooner.

Why the deductible matters

- A high deductible can make a low-premium plan feel more expensive when you need care

- A lower deductible can reduce upfront medical spending during the year

- The best choice depends on how often you expect to use covered services

Copay vs. Coinsurance: What Is the Difference?

Copays and coinsurance are both forms of cost-sharing, but they work differently. A copay is usually a fixed dollar amount for a service, while coinsurance is a percentage of the allowed cost after the deductible is met for services where coinsurance applies.[1]

This difference can change your risk. Copays are easier to predict because the amount is set in advance. Coinsurance can be harder to estimate because the dollar amount depends on the cost of the service itself. That is one reason shoppers should review the Summary of Benefits and Coverage instead of assuming that all cost-sharing works the same way from plan to plan.[5]

Simple rule

Copay means a set amount. Coinsurance means a percentage. If you expect expensive care, coinsurance can have a bigger effect on your total yearly spending than many people realize.

What the Out-of-Pocket Maximum Really Protects You From

The out-of-pocket maximum is the most you pay in a plan year for covered in-network services before the plan pays 100% of covered costs for the rest of that year. This limit is one of the most important protections in a major medical policy because it places a ceiling on covered in-network medical spending.[1]

That does not mean every medical expense automatically counts toward that limit. Premiums do not count, and out-of-network care or non-covered services may not count either. That is why two plans with similar premiums can still create very different worst-case financial exposure.

Why this number matters so much

The out-of-pocket maximum helps define the most you could owe for covered in-network care in a bad medical year. When you compare plans, this number can matter almost as much as the premium because it helps show your maximum financial risk.

A smart comparison looks at all three together: deductible, coinsurance, and out-of-pocket maximum. If you want a broader look at plan structure after that, our guide to major medical insurance plans can help you compare how different plan setups affect real-world cost.

How Plan Category Changes Cost

Bronze, Silver, Gold, and Platinum categories show how you and the plan share costs. These categories do not measure quality. In general, Bronze plans have lower monthly premiums and higher out-of-pocket costs, while Gold and Platinum plans usually have higher premiums and lower cost-sharing when you use care.[3]

If available in your area, Catastrophic plans are separate from the standard metal levels. For 2026, all Bronze and Catastrophic Marketplace plans are eligible to be used with Health Savings Accounts.[3] If provider flexibility matters to you, compare cost with plan structure too. Our guide to major medical insurance plans can help with that side of the decision.

How Subsidies and Savings Change the Real Cost

The sticker price is not always the price you actually pay. Some people qualify for premium tax credits that lower their monthly premium, and some also qualify for cost-sharing reductions that lower deductibles, copayments, and coinsurance. Cost-sharing reductions are available only if you enroll in a Silver plan.[4]

CMS also reported that the average HealthCare.gov premium after tax credits is projected to be $50 per month for the lowest-cost plan in 2026 for eligible enrollees. That does not mean everyone will pay $50. It does mean subsidy eligibility can completely change what a plan really costs.[4]

Cost rule that matters most

A plan should be compared after any subsidy or cost-sharing help you qualify for, not before. That is especially important for people buying their own coverage.

How to Lower Major Medical Insurance Costs

- Compare total yearly cost, not just premium

- Use in-network providers whenever possible

- Check your drug formulary before enrolling

- Review whether a Bronze, Silver, Gold, Platinum, or Catastrophic plan matches your expected usage

- Use the Summary of Benefits and Coverage and compare plans side by side

If you are still narrowing your choices, it also helps to compare Obamacare / ACA.

When You Can Shop and Why Timing Matters

Open Enrollment on HealthCare.gov runs from November 1 to January 15. Outside that window, you generally need a qualifying life event for a Special Enrollment Period, although Medicaid and CHIP can be available year-round.[5]

Timing matters for cost because missing the right enrollment window can limit your options or delay coverage. If you have a life change, it is worth checking whether you qualify for a Special Enrollment Period instead of assuming you have to wait.

Bottom Line

The cost of major medical insurance is the total financial picture, not the premium alone. A smart comparison includes monthly premium, deductible, coinsurance, out-of-pocket maximum, provider network, and any savings you qualify for. The best-cost plan is the one that fits both your budget and your real expected use of care.

References

-

HealthCare.gov, Out-of-pocket maximum/limit and Your total costs for health care: Premium, deductible, and out-of-pocket costs.

https://www.healthcare.gov/glossary/out-of-pocket-maximum-limit/ |

https://www.healthcare.gov/choose-a-plan/your-total-costs/

↩ -

HealthCare.gov, How insurance companies set health premiums.

https://www.healthcare.gov/how-plans-set-your-premiums/

↩ -

HealthCare.gov, Health plan categories: Bronze, Silver, Gold & Platinum and More plans now work with Health Savings Accounts.

https://www.healthcare.gov/choose-a-plan/plans-categories/ |

https://www.healthcare.gov/hsa-options/

↩ -

HealthCare.gov, How to save money on monthly health insurance premiums and Cost-sharing reductions; CMS, Plan Year 2026 Marketplace Plans and Prices Fact Sheet.

https://www.healthcare.gov/lower-costs/save-on-monthly-premiums/ |

https://www.healthcare.gov/lower-costs/save-on-out-of-pocket-costs/ |

https://www.cms.gov/newsroom/fact-sheets/plan-year-2026-marketplace-plans-prices-fact-sheet

↩ -

HealthCare.gov, 3 things to know before you pick a health insurance plan and When can you get health insurance?.

https://www.healthcare.gov/choose-a-plan/comparing-plans/ |

https://www.healthcare.gov/quick-guide/dates-and-deadlines/

↩