By MajorMedicalInsurance.com Editorial Team

Published on April 18, 2026 · Updated on April 19, 2026

Temporary Health Coverage Guide

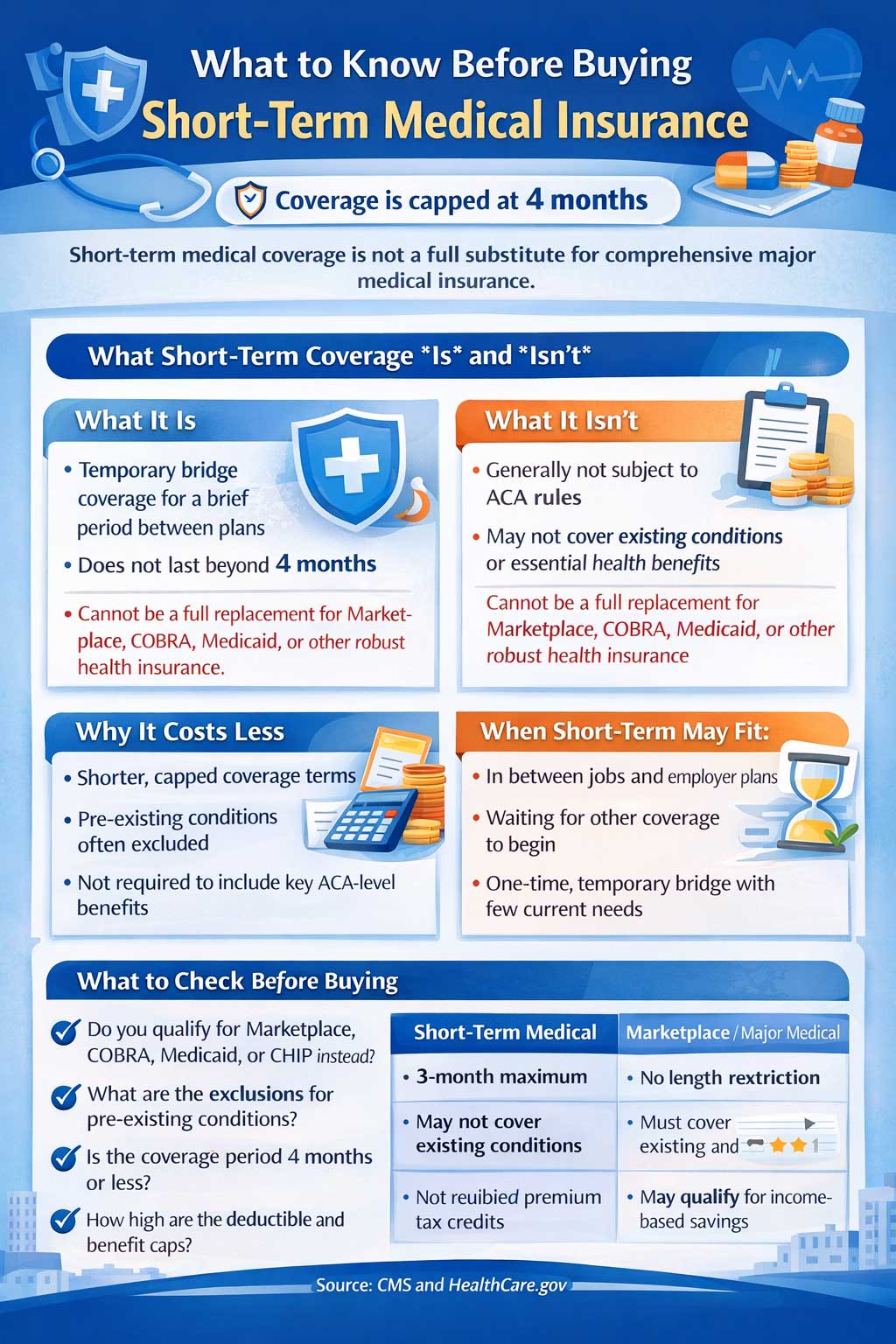

Short-term medical insurance, often called short-term limited-duration insurance, is designed to help fill a temporary gap in coverage rather than replace comprehensive health insurance for the long run.[1] Federal rules now limit these plans to an initial term of no more than 3 months and a total maximum coverage period of 4 months, including renewals or extensions.[2]

What it is

A temporary policy meant to bridge short coverage gaps, not serve as a full substitute for ACA-compliant major medical coverage.[1]

What it is not

It is generally not built under the same federal consumer protections that apply to comprehensive Marketplace coverage.[1][3]

Why people consider it

It may appeal to people between jobs or waiting for another source of coverage to begin.[1]

What to do first

Before buying one, check whether you qualify for Marketplace coverage, a Special Enrollment Period, COBRA, Medicaid, CHIP, or another employer-based option.[5]

What short-term medical insurance really means

Short-term medical coverage can look attractive because the monthly premium is often lower than a comprehensive major medical plan. The trade-off is that the policy is not built to the same standard as Marketplace coverage. That means you should not assume it covers pre-existing conditions, all essential health benefits, or the same level of cost protection that ACA-compliant plans provide.[1][3]

In other words, short-term medical insurance can be useful in narrow situations, but it works best when you treat it as temporary, limited coverage and read the exclusions closely. People who need broader protection for ongoing care, prescription costs, maternity needs, or chronic conditions usually need to compare it against stronger options such as major medical insurance plans or other comprehensive coverage first.

Short-term medical vs. comprehensive coverage

When short-term medical may make sense

- You are between health plans and need a very short bridge.[1]

- You are waiting for new employer coverage to begin and need temporary protection.

- You want some limited financial protection for a narrow time period while you finalize long-term coverage.

When it is usually the wrong fit

- You have an ongoing condition and need dependable coverage for pre-existing care.[1][3]

- You need comprehensive benefits such as maternity, mental health treatment, prescription coverage, or broader preventive care protections.[3]

- You want stronger overall consumer protection and predictable long-term coverage.

- You may qualify for Marketplace coverage, COBRA, Medicaid, CHIP, or another comprehensive alternative instead.[5]

What people often misunderstand

Lower premiums do not automatically mean better value. Short-term medical plans can cost less because they are not built to the same comprehensive standard as Marketplace plans. A cheaper monthly payment can still leave you more exposed if the policy excludes a condition, limits a benefit category, or provides less protection than an ACA-compliant plan.[1][3]

The most useful comparison is not premium alone. It is premium plus exclusions, deductible, coinsurance, network rules, prescription handling, and what happens if you need expensive care during the time you are insured.

What to check before buying a short-term policy

- Check whether you qualify for a Special Enrollment Period before you shop for short-term coverage.[5]

- Read the policy’s exclusions carefully, especially around pre-existing conditions and high-cost services.[1]

- Verify the exact coverage period so you do not confuse a short bridge with a long-term solution.[2]

- Review the deductible, coinsurance, benefit caps, and whether the provider network is limited.

- Do not assume prescription drugs, maternity care, mental health care, or preventive care will work the same way they do under an ACA-compliant plan.[3]

- Compare the policy against a real comprehensive alternative before deciding.

Smarter alternatives to compare first

Before choosing short-term medical insurance, many shoppers should compare it with Marketplace coverage, COBRA, Medicaid, CHIP, or a spouse’s or employer’s coverage if available.[5] On this site, it also makes sense to compare temporary coverage against stronger long-term options such as major medical insurance for individuals and ACA coverage.

The goal is not to assume short-term coverage is always wrong. It is to compare it honestly against the broader protection you may still be able to access.

Bottom line

Short-term medical insurance can play a limited role when you are truly in transition and need a brief bridge. It is far less suitable as a long-term replacement for comprehensive health insurance. The most responsible approach is to treat it as a temporary, carefully reviewed option only after you have checked for Marketplace eligibility, Special Enrollment rights, COBRA, Medicaid, CHIP, and other comprehensive alternatives.[1][5]

References

- CMS — Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage ↩

- Federal Register — Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage ↩

- HealthCare.gov — What Marketplace Health Insurance Plans Cover | HealthCare.gov — Marketplace Health Plans Cover Pre-Existing Conditions ↩

- HealthCare.gov — Out-of-Pocket Maximum/Limit ↩

- HealthCare.gov — Marketplace Coverage When You’re Unemployed | CMS — Special Enrollment Periods (SEP) Job Aid ↩

MajorMedicalInsurance.com Editorial Team

This article was prepared using current CMS, Federal Register, and HealthCare.gov materials to help readers understand how short-term medical insurance works, where it may fit, and where it falls short compared with comprehensive coverage. It is intended for educational purposes and should be used alongside official plan documents and licensed guidance when comparing health coverage.

Reviewed for clarity, consumer usefulness, and alignment with current public health coverage guidance.