By MajorMedicalInsurance.com Editorial Team

Published on · Updated on

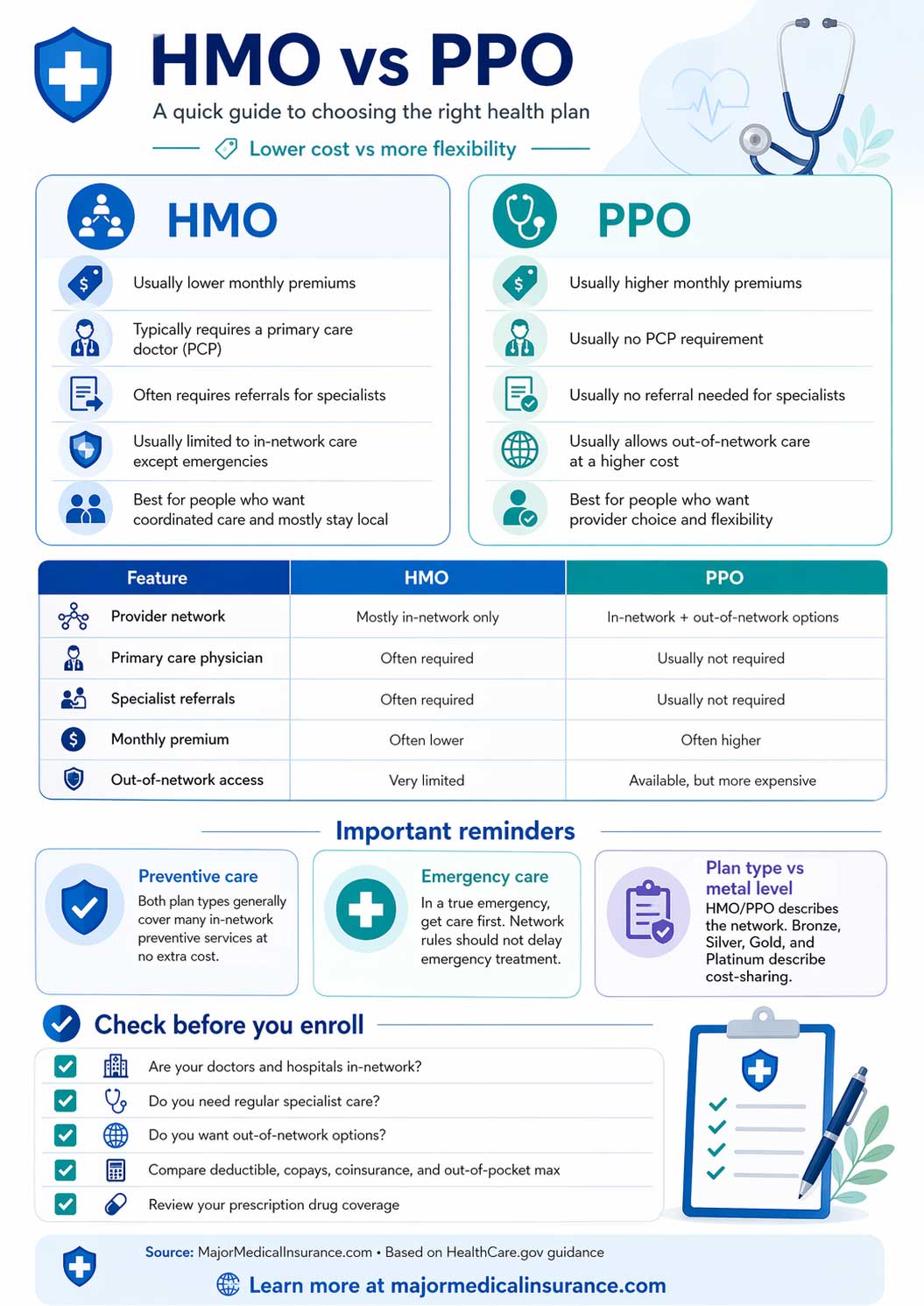

Choosing between an HMO and a PPO is one of the most important steps in picking a health plan. Both can be part of comprehensive major medical health insurance, but they work differently when it comes to provider access, referrals, out-of-network care, and total cost.

Quick Answer

In general, an HMO is usually more restrictive but often lower-cost, while a PPO usually offers more freedom to choose providers but often costs more. The best choice depends on whether you value lower premiums and coordinated care or broader provider access and fewer referral rules.

What an HMO and a PPO Actually Mean

An HMO is a Health Maintenance Organization. HealthCare.gov says HMOs usually limit coverage to care from doctors who work for or contract with the HMO, and they generally do not cover out-of-network care except in an emergency. HMOs often provide integrated care and focus on prevention and wellness.[1]

A PPO is a Preferred Provider Organization. HealthCare.gov says PPOs contract with a network of providers but usually let you use doctors, hospitals, and specialists outside the network too, usually at a higher cost. PPOs generally do not require referrals to see specialists.[1]

This is why HMO vs PPO is not really about which one is “better” in the abstract. It is about which tradeoff fits your real life. If you are still comparing the larger structure of coverage, you may also want to review major medical insurance plans and major medical insurance PPOs.

HMO vs PPO at a Glance

Why HMOs Often Cost Less

HMOs often appeal to people who want a lower monthly premium and more coordinated care. Because the network is narrower and referrals are commonly part of the plan structure, HMOs can be easier for insurers to manage and often cost less than more flexible designs. That lower premium can be attractive for families and individuals who usually use local in-network care and do not mind working through a primary care doctor.

An HMO may fit you better if:

- You want lower monthly premiums

- You are comfortable choosing a primary care doctor

- You usually stay local for care

- You do not expect to need many out-of-network specialists

- You like a more coordinated, managed-care structure

Why PPOs Often Cost More

PPOs usually cost more because they give you more freedom. You can often see specialists without a referral, and you usually have some coverage outside the network, although it will generally cost more than staying in network. That flexibility can be valuable for people with complex care needs, those who travel often, or those who want access to a broader provider pool.

A PPO may fit you better if:

- You want broader provider choice

- You do not want referrals for specialists

- You have doctors or facilities outside one narrow network

- You travel often or split time between locations

- You are willing to pay more for flexibility

How Preventive Care Fits In

One thing HMO and PPO shoppers sometimes miss is that preventive care rules do not depend only on the network type. HealthCare.gov says preventive services are generally covered at no cost to you when provided by an in-network medical provider, and in many cases you do not pay copayments or coinsurance for certain preventive services even if you have not met your deductible. Coverage can vary by situation, so “free” should not be treated as universal for every service, but preventive care is still an important benefit in both HMO and PPO major medical plans.[2]

If virtual care matters to you, it is also worth checking whether your plan includes useful telemedicine access, since that can affect convenience as much as network type does.

Emergency Care Is Different

Emergency care is one of the biggest areas where people misunderstand network rules. HealthCare.gov says insurers cannot require prior approval before you get emergency room services from a provider or hospital outside your plan’s network.[3] CMS also says the No Surprises Act bans surprise bills for most emergency services and bans out-of-network cost-sharing for most emergency and some non-emergency services, meaning you generally cannot be charged more than in-network cost-sharing for those protected situations.[3]

Important emergency rule

In a true emergency, go get care. Do not delay emergency treatment because you are trying to sort out whether the hospital is in-network first.

HMO vs PPO Is Separate From Bronze, Silver, Gold, and Platinum

Another common confusion is mixing up network type with plan category. HMO and PPO describe how the network works. Bronze, Silver, Gold, and Platinum describe how you and the plan split costs. HealthCare.gov treats these as separate parts of the decision, which is why someone can compare plan type and plan category at the same time.[4]

That means you are not choosing between “HMO or Silver.” You might be choosing between something like a Silver HMO and a Gold PPO. That difference can matter a lot when comparing total cost and provider flexibility.

How to Compare HMO and PPO Plans the Smart Way

HealthCare.gov recommends comparing total costs, plan documents, provider networks, and covered prescription drugs when choosing a plan. That is especially important for HMO vs PPO decisions, because the wrong network setup can make a plan look cheaper than it really is for your situation.[5]

Check these before enrolling

- Whether your doctors and hospitals are in-network

- Whether you are comfortable using a primary care doctor as a gatekeeper

- Whether you need regular specialist care

- Whether you want any out-of-network option

- The deductible, copays, coinsurance, and out-of-pocket maximum

- Your prescription drug formulary

If you are comparing major medical options more broadly, major medical insurance benefits can help you connect the plan structure to real-world coverage value.

Bottom Line

An HMO often works best for people who want lower premiums, local in-network care, and a coordinated system built around a primary care doctor. A PPO often works best for people who want more provider freedom, fewer referral barriers, and some out-of-network access even if it costs more. The right choice depends less on which label sounds better and more on how you actually use healthcare.

References

-

HealthCare.gov, Health insurance plan & network types: HMOs, PPOs, and more.

https://www.healthcare.gov/choose-a-plan/plan-types/

↩ -

HealthCare.gov, Preventive health services.

https://www.healthcare.gov/coverage/preventive-care-benefits/

↩ -

HealthCare.gov, Getting emergency care; CMS, No Surprises: Understand your rights against surprise medical bills.

https://www.healthcare.gov/using-marketplace-coverage/getting-emergency-care/ |

https://www.cms.gov/newsroom/fact-sheets/no-surprises-understand-your-rights-against-surprise-medical-bills

↩ -

HealthCare.gov, Health plan categories: Bronze, Silver, Gold & Platinum.

https://www.healthcare.gov/choose-a-plan/plans-categories/

↩ -

HealthCare.gov, 3 things to know before you pick a health insurance plan.

https://www.healthcare.gov/choose-a-plan/comparing-plans/

↩