By MajorMedicalInsurance.com Editorial Team

Published on April 19, 2026 · Updated on April 19, 2026

Coverage Guide

Pre-existing conditions do not block you from getting ACA-compliant major medical coverage. In today’s U.S. Marketplace, insurers cannot reject you, charge you more, or refuse to cover essential health benefits because of a condition you had before coverage started.[1][2]

Quick answer

ACA-compliant major medical plans must cover treatment for pre-existing conditions and cannot charge more based on your health history.[1][2]

What still changes price

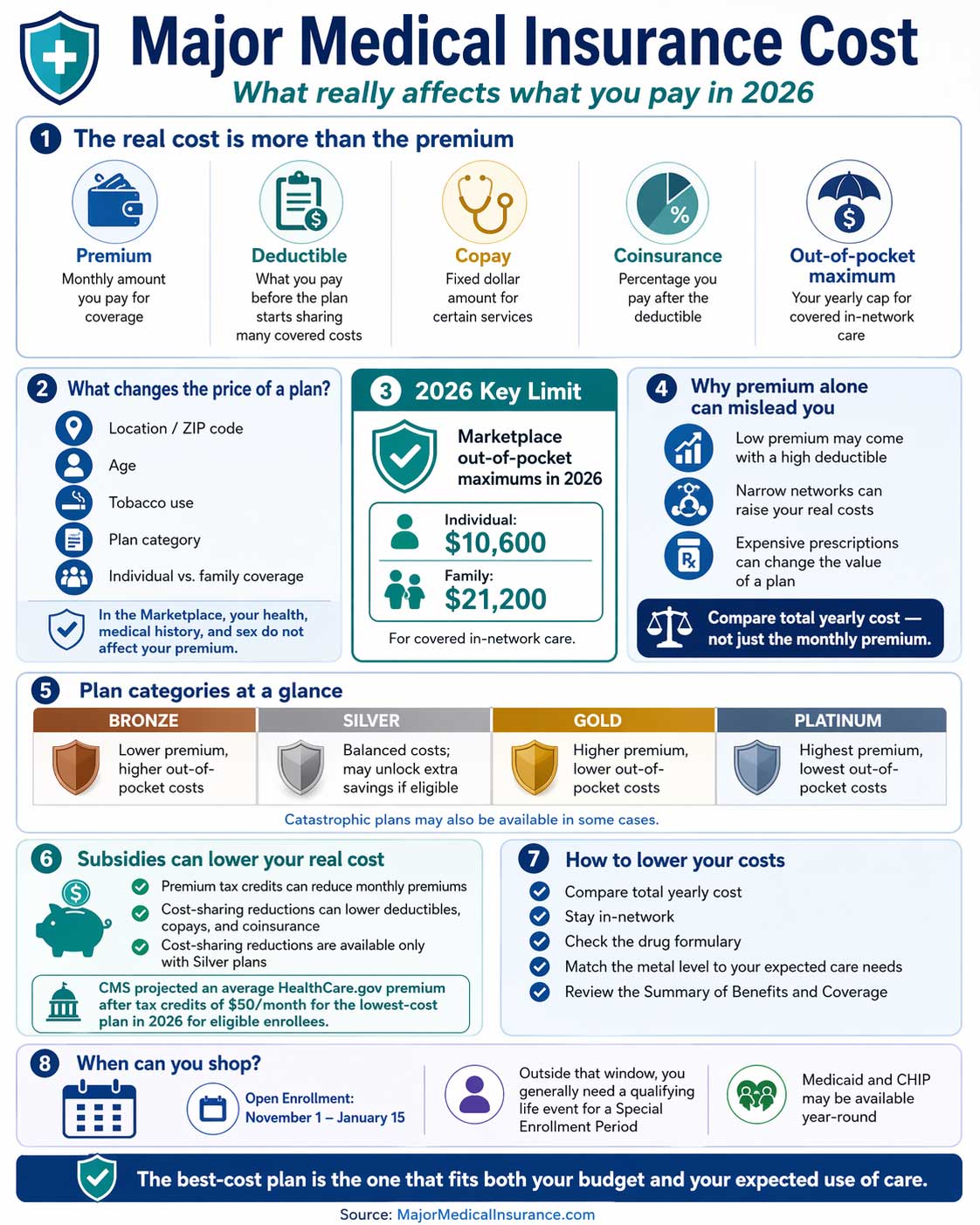

Marketplace premiums can vary by location, age, tobacco use, plan category, and whether dependents are covered, but not by medical history.[2]

When to enroll

You can enroll during Open Enrollment or after certain qualifying life events, including losing health coverage.[3]

What to avoid assuming

Not every health product follows the same rules. Short-term plans are not subject to the ACA’s core protections for pre-existing conditions.[4]

What counts as a pre-existing condition?

In plain language, a pre-existing condition is a health issue you had before new coverage starts. That could include something ongoing, such as asthma, diabetes, high blood pressure, arthritis, depression, cancer history, or another condition that requires monitoring, prescriptions, specialist care, or recurring treatment. For consumers shopping for comprehensive coverage, the most important point is not whether the condition has a label. It is whether the new plan can legally use that condition against you.

Under current Marketplace rules, ACA-compliant coverage must cover treatment for pre-existing conditions. If you want the broader foundation first, compare this with major medical health insurance and Obama Care / ACA.[1]

Does major medical insurance cover pre-existing conditions?

For ACA-compliant individual and Marketplace coverage, yes. HealthCare.gov states that Marketplace plans must cover treatment for pre-existing medical conditions. Insurers cannot reject you, charge you more, or refuse to pay for essential health benefits because of a condition you had before coverage started.[1]

That protection is one of the biggest reasons comprehensive major medical coverage is different from narrower or lower-quality products. It means people shopping for serious health coverage should focus less on whether their condition makes them “uninsurable” and more on whether the plan’s network, prescriptions, deductible, and out-of-pocket exposure actually fit their medical needs.

What still matters even with ACA protection

“Covered” does not mean every plan works equally well for chronic or ongoing care. A plan can comply with pre-existing condition rules and still be a poor fit if your doctors are out of network, your medications sit in expensive tiers, or the deductible is too high for the way you use care.

What can still affect your premium?

Health history is not one of the factors that can set a Marketplace premium. HealthCare.gov says premiums can vary based on location, age, tobacco use, plan category, and whether the plan covers dependents.[2] That means two people can see different prices even when neither is being rated based on a pre-existing condition.

Price factors that can apply

- ZIP code or rating area

- Age

- Tobacco use

- Plan category

- Whether dependents are covered[2]

What cannot set the premium

- Your medical history

- Your diagnosis history

- Your current health condition

- Your sex[2]

How to shop for major medical coverage if you have ongoing health needs

If you have a chronic condition or need regular treatment, the smartest comparison is not just premium. It is premium plus network, prescription coverage, specialist access, deductible, coinsurance, and annual out-of-pocket exposure. Our guide to major medical insurance cost can help with that broader decision.

Practical shopping rule

If you expect regular prescriptions, therapy, specialist visits, imaging, infusions, or follow-up care, a higher-premium plan can still be the better value if it lowers your real treatment costs and gives you better network access.

When can you enroll?

Open Enrollment is the main annual window, but many people can enroll outside it through a Special Enrollment Period. HealthCare.gov says losing qualifying health coverage is one of the life events that can make you eligible for a Special Enrollment Period.[3] If you are timing coverage around a job change or another transition, compare this with major medical insurance enrollment.

Common SEP examples

- Losing qualifying health coverage

- Moving

- Getting married

- Having a baby or adopting a child[3]

Why short-term plans are not the same thing

This is where many shoppers get into trouble. Short-term, limited-duration insurance is not subject to the ACA’s core consumer protections for pre-existing conditions.[4] That means a person who needs strong protection for ongoing care should be careful not to treat a short-term plan as equivalent to ACA-compliant major medical coverage.

If you want the differences laid out more directly, see short-term medical. For shoppers with real pre-existing condition concerns, the safer baseline is usually comprehensive major medical coverage rather than a temporary gap product.

Common mistakes to avoid

- Assuming “covered” means every plan handles your doctors, drugs, and treatment the same way.

- Shopping only by premium instead of total yearly cost.

- Ignoring the provider directory until after enrollment.

- Ignoring formulary tiers and prior authorization rules for regular medications.

- Assuming a short-term or limited-benefit product gives the same protection as ACA-compliant major medical coverage.

Bottom line

Pre-existing conditions do not prevent you from getting ACA-compliant major medical insurance, and they should not increase your Marketplace premium or block essential health benefit coverage.[1][2] The real job is choosing the right plan structure: network, prescriptions, deductible, out-of-pocket maximum, and enrollment timing. For people managing ongoing health needs, that practical comparison matters more than fear of being denied.

References

- HealthCare.gov — Marketplace Health Plans Cover Pre-Existing Conditions ↩

- HealthCare.gov — How Insurance Companies Set Health Premiums ↩

- HealthCare.gov — Special Enrollment Period | HealthCare.gov — Qualifying Life Event ↩

- CMS — Final Rule Limiting Short-Term Plans and Explaining They Are Not Subject to ACA Core Consumer Protections ↩

- HealthCare.gov — What Marketplace Health Insurance Plans Cover ↩