By MajorMedicalInsurance.com Editorial Team

Published on · Updated on

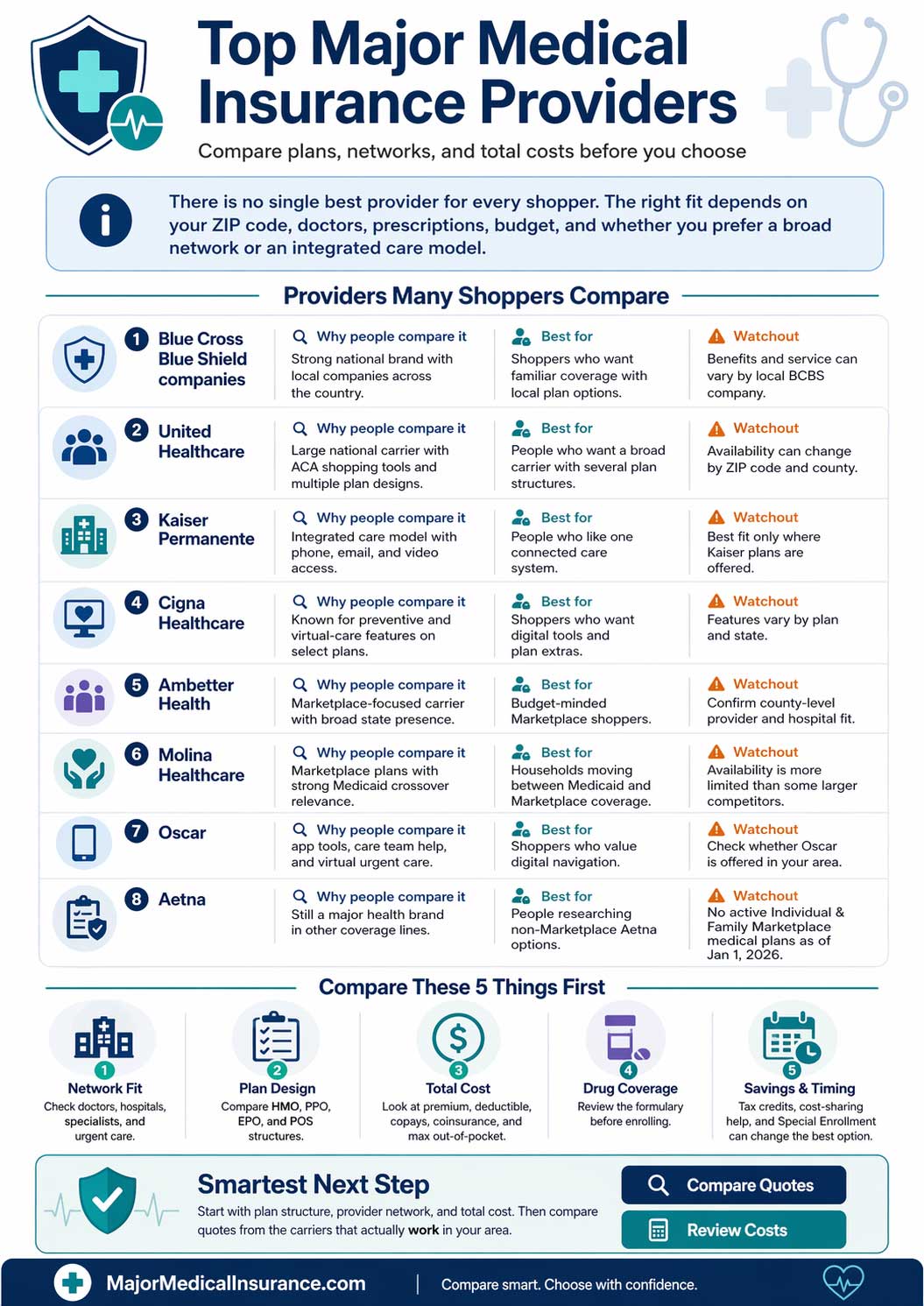

There is no single best major medical insurance provider for every shopper. The strongest option depends on your ZIP code, county, doctors, prescriptions, budget, and whether you prefer a broad provider network, an integrated care model, or a lower-premium Marketplace plan.[1] [2]

That is why the smartest way to compare insurers is to start with plan structure, network type, and total out-of-pocket exposure before you focus on brand names. If you want the foundation first, review our guides to major medical health insurance, major medical insurance plans, and medical plans HMO vs. PPO.

Quick Summary

The major insurers many shoppers compare most often include Blue Cross Blue Shield companies, UnitedHealthcare, Kaiser Permanente, Cigna Healthcare, Ambetter Health, Molina Healthcare, and Oscar. Aetna remains a major health brand in other lines of coverage, but it says its Individual & Family Marketplace medical plans are no longer active as of January 1, 2026.[6] [5] [7] [8] [9] [10] [11] [12]

What Makes a Provider “Top” for Your Situation

A provider is only “top-tier” if its plans actually fit your medical and financial needs. When comparing insurers, focus on these five areas first:

- Network fit: Make sure your doctors, hospitals, specialists, and nearby urgent care centers are in-network whenever possible.[1]

- Plan design: Compare HMO, PPO, EPO, and POS structures instead of assuming one logo automatically means better coverage.[1]

- Total cost: Monthly premium matters, but deductible, copays, coinsurance, and the annual out-of-pocket maximum matter just as much.[2]

- Drug coverage: Check the formulary before enrolling if you take regular prescriptions.

- Savings and timing: Premium tax credits, cost-sharing reductions, and Special Enrollment rules can completely change which plan is best for you.[3] [4]

If cost is your main concern, also review major medical insurance cost, major medical insurance eligibility, and major medical insurance enrollment before requesting quotes.

Major Medical Providers Many Shoppers Compare

| Provider | Why Shoppers Look At It | Often Best For | Key Watchout |

|---|---|---|---|

| Blue Cross Blue Shield companies | Strong national brand with local companies across the country[6] | Shoppers who want a familiar system with local plan options | Benefits and service can vary by local BCBS company[6] |

| UnitedHealthcare | Current Individual & Family ACA plan shopping tools and enrollment guidance[5] | People who want multiple plan designs and a large national carrier | Availability can change by ZIP code and county[5] |

| Kaiser Permanente | Integrated care model with phone, email, and video access[7] | People comfortable using one connected care system | Best fit only where Kaiser individual and family plans are offered[7] |

| Cigna Healthcare | Individual/family plans with strong preventive and virtual-care features on select plans[8] | Shoppers who want digital tools and plan extras where available | Features vary by plan and state[8] |

| Ambetter Health | Marketplace-focused carrier with plans in 29 states[9] | Budget-minded Marketplace shoppers who want broad state presence | You still need to confirm county-level plan and provider fit[9] |

| Molina Healthcare | Marketplace plans in nine states and strong Medicaid/Marketplace crossover presence[10] | Households moving between Medicaid and Marketplace coverage | State availability is more limited than some larger competitors[10] |

| Oscar | Individual/family plans with an app, care team, and virtual urgent care tools[11] | Tech-forward shoppers who value digital navigation | Check whether Oscar is offered in your service area[11] |

| Aetna | Still a major health brand across employer, Medicare, Medicaid, dental, vision, student, and international coverage lines[12] | People researching non-Marketplace Aetna options | Not a current Individual & Family Marketplace medical option for new shoppers in 2026[12] |

Provider-by-Provider Breakdown

Blue Cross Blue Shield Companies

Blue Cross Blue Shield is one of the most recognizable names in U.S. health coverage, but it is important to understand that BCBS is a system of local companies rather than a single standardized insurer everywhere. The Blue Cross Blue Shield Association says BCBS companies offer a personalized local approach across the country, which helps explain why shoppers often start there when they want broad brand recognition and strong local market presence.[6]

The biggest advantage is familiarity and reach. The biggest caution is that benefits, networks, and member experience can vary depending on the local BCBS company serving your state or region. If you are comparing Blue plans specifically, use our page on major medical insurance Blue Cross.

UnitedHealthcare

UnitedHealthcare remains one of the most important carriers to compare if you are shopping for current ACA coverage. Its official Individual & Family pages emphasize Marketplace plan shopping, enrollment guidance, plan-type comparisons, and the fact that availability depends on where you live.[5]

That makes UnitedHealthcare a strong starting point for shoppers who want a large national carrier and a range of plan designs, but not every ZIP code or county will have UHC individual and family options. Before choosing it, verify provider participation, prescription coverage, and how the plan handles referrals and out-of-network care.

Kaiser Permanente

Kaiser Permanente stands out because it combines coverage with a connected care delivery model. Kaiser highlights phone, email, and video access, preventive care, and flexible individual and family plans.[7]

This can work very well for people who like the idea of a coordinated care system rather than a looser independent network. The tradeoff is simple: Kaiser is strongest when you are in a service area where its system is available and you are comfortable using that model for most of your care.

Cigna Healthcare

Cigna’s current individual and family pages highlight preventive care, virtual care, customer support, and certain select-plan features such as low-cost generics or lower-cost routine care structures.[8] That makes Cigna attractive to shoppers who want a modern member experience and are comparing day-to-day usage features, not just catastrophic protection.

The key detail is that these features are not identical across every plan. Always check the exact Summary of Benefits and Coverage, network, and formulary in your state before assuming a headline feature applies to the option you are considering.

Ambetter Health

Ambetter has become a major name for Marketplace shoppers because it says it offers coverage in 29 states and provides tools to shop by ZIP code, search providers, and manage coverage digitally.[9] For consumers who want ACA-compatible coverage with a wide state footprint, Ambetter often belongs on the shortlist.

Still, statewide presence is not the same as county-level fit. You should compare the hospital system, specialist availability, prescription coverage, and network design in your exact area before choosing a lower-premium option just because the brand is widely available.

Molina Healthcare

Molina says it offers Marketplace plans in nine states and positions itself clearly around Marketplace and Medicaid-related coverage paths.[10] That makes Molina especially relevant for households whose income, program eligibility, or coverage source may shift over time.

Its narrower footprint compared with some larger carriers does not automatically make it a worse choice. It simply means local validation matters more. Compare network access carefully and make sure the specific Molina plan available to you matches your expected medical usage.

Oscar

Oscar continues to market itself around digital navigation, highlighting its Oscar app, care team support, and virtual urgent care tools for individual and family shoppers.[11] That can be appealing if you want a plan that feels easier to manage through your phone and online account.

Oscar can be worth strong consideration when it is available in your area and the provider network works for your doctors and hospitals. As always, tech features are helpful, but they should not outweigh network fit or drug coverage if you rely on ongoing care.

Aetna

Aetna is still a major health insurance brand, but this is exactly where outdated articles go wrong. Aetna’s own site says that, as of January 1, 2026, it no longer offers, renews, or has active individual and family medical plans through the Health Insurance Marketplace in any U.S. state.[12]

That does not mean Aetna disappeared. It still points visitors to other coverage lines such as employer plans, Medicare, Medicaid, dental, vision, student, and international products.[12] But for a current Marketplace comparison article, Aetna should be treated as a legacy reference or a non-Marketplace option, not as a standard current ACA shopping choice. If you want a dedicated page on that brand context, see Aetna major medical insurance.

How to Compare Providers Without Making an Expensive Mistake

The safest comparison process is usually this: first compare network type, then metal level, then total cost, then prescriptions, and only after that compare brand reputation. HealthCare.gov makes clear that metal categories such as Bronze, Silver, Gold, and Platinum describe how costs are shared, not the quality of care itself.[2]

That is important because the “best” provider can still be the wrong choice if the plan has the wrong deductible structure, the wrong drug list, or the wrong specialist network for your health needs. If you may qualify for premium tax credits or other Marketplace savings, update your income and household information first so you compare plans using realistic net costs instead of sticker-price premiums alone.[3]

Ways to Save Without Choosing the Wrong Plan

- Compare the plan’s full cost, not just the monthly premium.

- Check whether you qualify for premium tax credits or other savings.[3]

- Use in-network doctors, labs, and hospitals whenever possible.[1]

- Review the drug formulary before enrolling.

- Use preventive care benefits and annual plan review windows to avoid drifting into a poor-fit plan.[4]

Compare the right way before you enroll

Start with plan structure, provider network, and total cost. Then narrow your list to the carriers that actually work in your area.

References

- HealthCare.gov — Health insurance plan and network types ↩ ↩ ↩ ↩

- HealthCare.gov — Health plan categories ↩ ↩ ↩

- HealthCare.gov — Saving money on health insurance premiums ↩ ↩ ↩

- HealthCare.gov — Special Enrollment Period ↩ ↩

- UnitedHealthcare — Individual and family health insurance plans ↩ ↩

- Blue Cross Blue Shield — The Blue Cross and Blue Shield System ↩ ↩ ↩ ↩

- Kaiser Permanente — Individual and family plans overview ↩ ↩ ↩ ↩

- Cigna Healthcare — Individual and Family Plan Benefits ↩ ↩ ↩ ↩

- Ambetter Health — Affordable health insurance plans ↩ ↩ ↩ ↩

- Molina Healthcare — About Marketplace ↩ ↩ ↩ ↩

- Oscar — Health insurance for individuals and families ↩ ↩ ↩ ↩

- Aetna — Individuals and families ↩ ↩ ↩ ↩ ↩

About the Author

Major Medical Insurance Editorial Team

This article was reviewed and updated using current public carrier pages and federal health coverage resources. It is intended for general educational purposes and should not replace official plan documents, Summary of Benefits and Coverage forms, or licensed advice tailored to your state and eligibility.