By MajorMedicalInsurance.com Editorial Team

Published on · Updated on

Major medical insurance is one of the most important types of health coverage in the United States, but eligibility can mean different things depending on how you get coverage. Some people qualify through an employer, others through the Health Insurance Marketplace, and others through public programs such as Medicare or Medicaid. The right path depends on your age, household situation, income, work status, and whether you already have access to other coverage.

Quick Answer

Eligibility for major medical insurance depends on the source of the plan. Marketplace coverage generally requires that you live in the United States, be a U.S. citizen or national or be lawfully present, and not be incarcerated. Employer coverage depends on your employer’s plan rules. Medicare and Medicaid follow their own federal and state eligibility rules. The most important step is to identify which coverage path actually applies to you before comparing plans.

What Major Medical Insurance Means

Major medical health insurance generally refers to comprehensive coverage designed to help pay for serious and routine medical needs, including hospitalization, physician services, emergency care, preventive services, prescription drugs, and other covered benefits. It is different from narrow or temporary products because it is designed to provide broader financial protection when care becomes expensive.

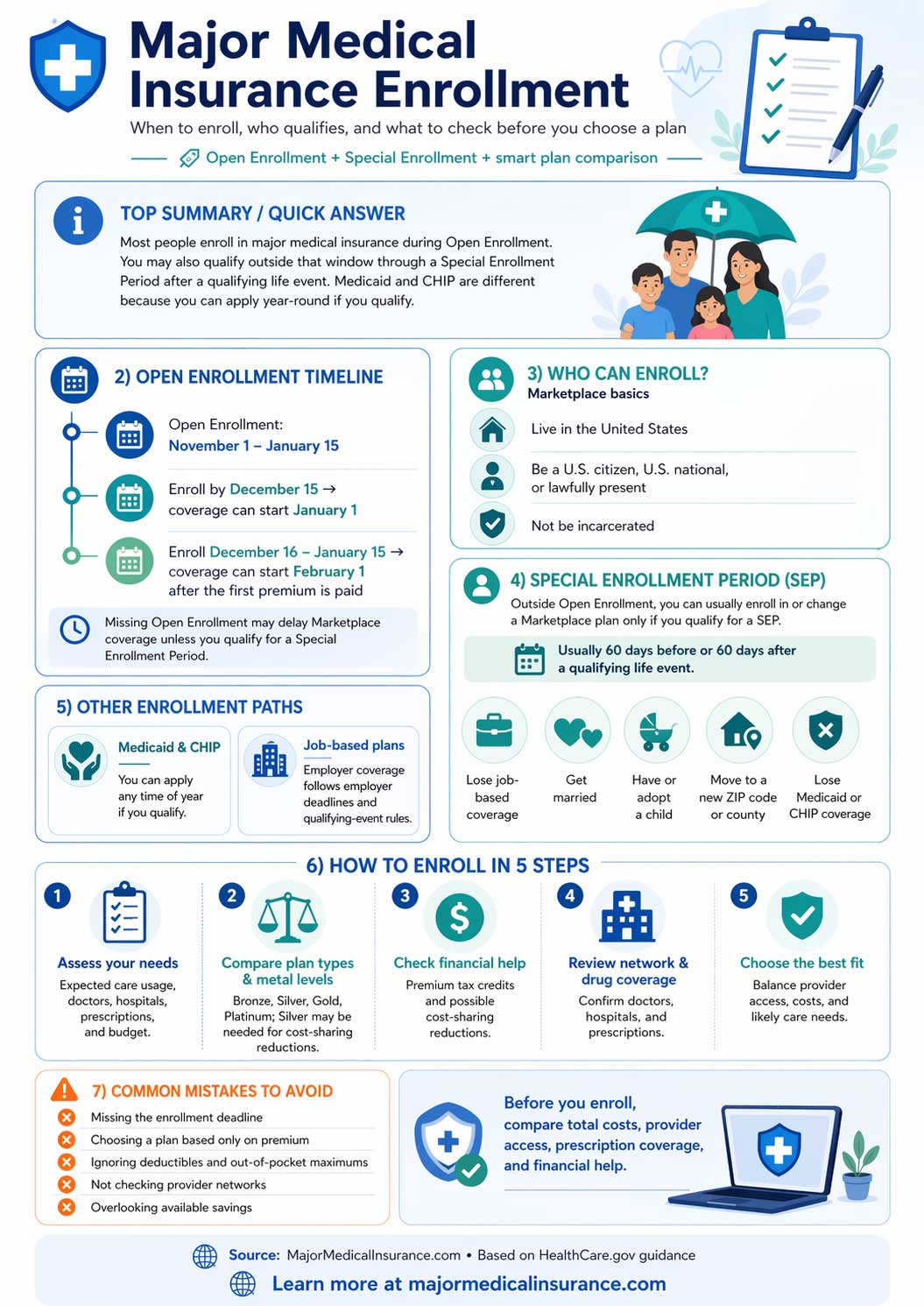

Marketplace Eligibility

If you are buying your own coverage, the Health Insurance Marketplace is often the first place to check. HealthCare.gov says that, in general, to enroll in Marketplace coverage you must live in the United States, be a U.S. citizen or national or be lawfully present, and not be incarcerated. It also states that if you already have Medicare, you cannot enroll in a Marketplace health plan.[1]

That is why people shopping on their own often end up comparing this topic with Obamacare / ACA and pre-existing conditions and major medical insurance.

When You Can Enroll

Eligibility is not only about who qualifies. It is also about timing. On HealthCare.gov, Open Enrollment runs from November 1 through January 15. If you miss that window, you usually need a qualifying life event to use a Special Enrollment Period.[1]

Common Special Enrollment triggers

- Losing job-based coverage

- Getting married

- Having or adopting a child

- Moving to a new service area

- Losing Medicaid or CHIP coverage

HealthCare.gov says SEP timing is usually 60 days before or after the qualifying event, although some Medicaid and CHIP loss situations can work differently.[1] For a deeper look at timing and sign-up windows, see major medical insurance enrollment.

Employer-Sponsored Coverage

Many Americans get major medical coverage through work, but the rules are not as simple as “all employers must offer insurance.” Employer eligibility depends on the employer’s plan rules, waiting periods, full-time or part-time classification, and whether dependents are eligible. Under the ACA employer shared responsibility rules, the large-employer requirements generally apply to applicable large employers with 50 or more full-time employees, including full-time equivalent employees.[2]

If you have an offer of job-based coverage, that can also affect whether you qualify for Marketplace savings. HealthCare.gov says that in 2026 a job-based plan is considered affordable if your share of the premium for the lowest-cost self-only plan is less than 9.96% of household income and the plan meets minimum value standards. In that case, you generally will not qualify for Marketplace savings.[2]

Medicare Eligibility

Medicare is a separate federal coverage path. Medicare.gov says people generally become eligible at age 65, after receiving Social Security disability benefits for 24 months, or earlier in certain cases such as ALS or ESRD.[3] If you are near Medicare age or already dealing with disability-based eligibility, it often makes more sense to compare that route directly with Medicare Advantage instead of treating every option as part of the same market.

Medicaid Eligibility

Medicaid eligibility is different because it varies by state and by coverage group. Medicaid.gov explains that federal law requires states to cover certain groups, including some low-income families, qualified pregnant women and children, and people receiving SSI, while states may also choose to cover other groups under additional options.[4]

HealthCare.gov also says you can apply for Medicaid and CHIP at any time during the year, which makes these programs different from the Marketplace Open Enrollment schedule.[4]

What Usually Affects Eligibility

What This Page Should Not Confuse With Eligibility

Eligibility is not the same thing as affordability, plan quality, or network fit. A person may be eligible for a plan and still need to compare whether it makes sense based on deductible, provider network, prescription coverage, and total out-of-pocket risk.

Bottom Line

Major medical insurance eligibility depends first on where the coverage comes from. Marketplace coverage, employer plans, Medicare, and Medicaid all use different rules. The smartest approach is to identify your path first, then compare the plans you can actually access, instead of assuming one set of eligibility rules applies to every type of coverage.

References

-

HealthCare.gov, Are you eligible to use the Marketplace?, When can you get health insurance?, and Special Enrollment Period.

https://www.healthcare.gov/quick-guide/eligibility/ |

https://www.healthcare.gov/quick-guide/dates-and-deadlines/ |

https://www.healthcare.gov/coverage-outside-open-enrollment/special-enrollment-period/

↩ -

IRS, Employer shared responsibility provisions; HealthCare.gov, If you have job-based insurance and Affordable coverage.

https://www.irs.gov/affordable-care-act/employers/employer-shared-responsibility-provisions |

https://www.healthcare.gov/have-job-based-coverage/ |

https://www.healthcare.gov/glossary/affordable-coverage/

↩ -

Medicare.gov, Get started with Medicare, Which path is right for me?, and End-Stage Renal Disease (ESRD).

https://www.medicare.gov/basics/get-started-with-medicare |

https://www.medicare.gov/basics/get-started-with-medicare/other-paths |

https://www.medicare.gov/basics/end-stage-renal-disease

↩ -

Medicaid.gov, Eligibility Policy; HealthCare.gov, Medicaid & CHIP coverage.

https://www.medicaid.gov/medicaid/eligibility-policy |

https://www.healthcare.gov/medicaid-chip/

↩