By MajorMedicalInsurance.com Editorial Team

Published on · Updated on

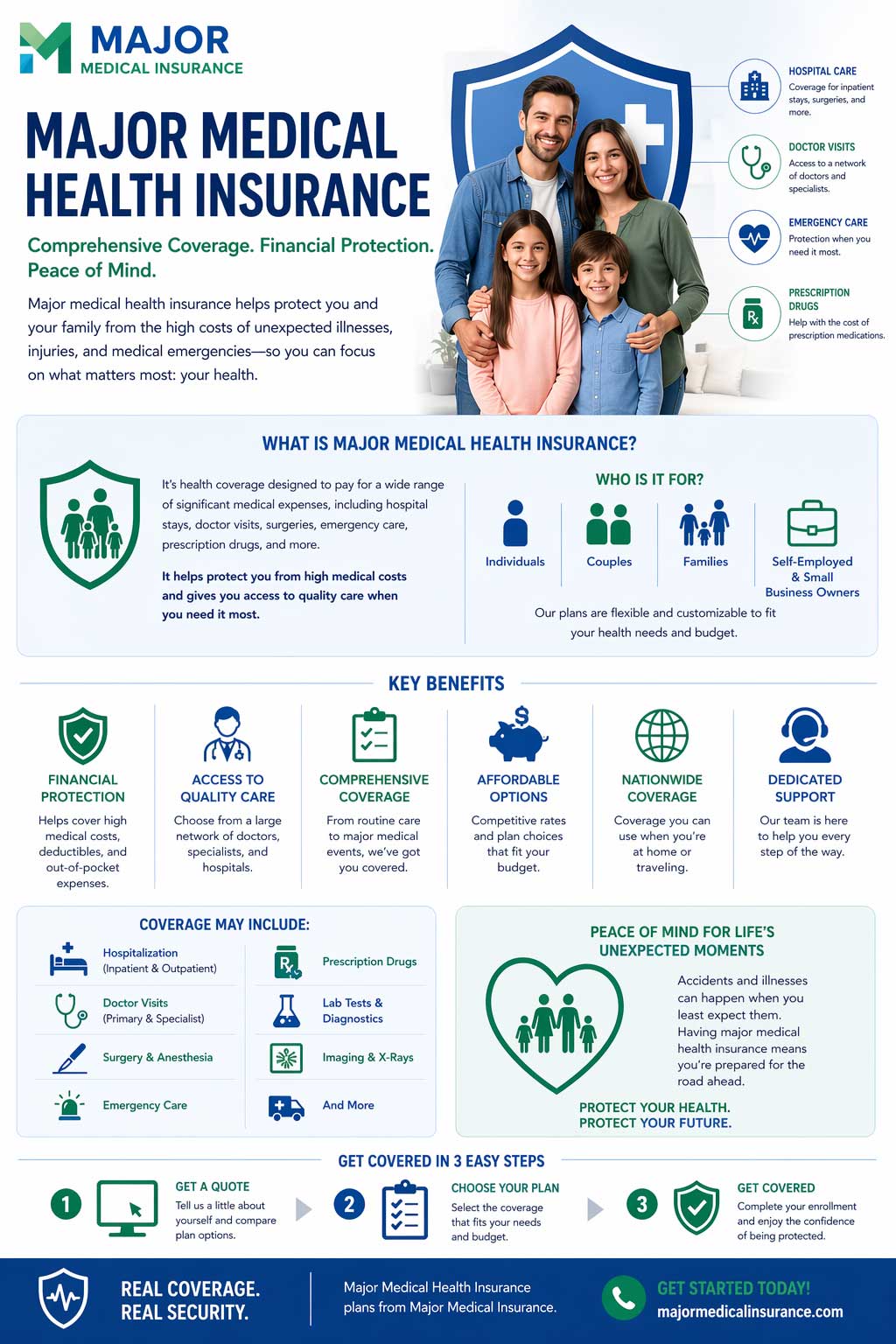

Major medical health insurance is the type of coverage most people mean when they talk about “real” health insurance. It is designed to help pay for a broad range of medically necessary care, including hospital treatment, physician services, prescription drugs, preventive care, emergency care, maternity care, mental health treatment, and more. In today’s market, that usually means comprehensive coverage rather than a narrow cash-benefit or temporary policy.[1]

If you are shopping for coverage under the Affordable Care Act, start with our Obama Care ACA guide. If you want a deeper breakdown of benefits, also read what major medical insurance covers. And if you are comparing how network structure affects flexibility, our guide to medical plans HMO vs PPO can help before you choose a plan.

Quick Answer

A strong major medical plan is built to protect you from high medical bills while giving you access to broad, ongoing healthcare. Marketplace plans cover essential health benefits, must cover treatment for pre-existing conditions, and generally include certain in-network preventive services at no extra cost to you.[1] [2]

What Major Medical Health Insurance Usually Covers

Comprehensive major medical coverage is built around broad protection rather than a limited payout. Under current Marketplace rules, plans must cover 10 categories of essential health benefits, including hospitalization, outpatient care, emergency services, prescription drugs, maternity and newborn care, mental health and substance use treatment, laboratory services, rehabilitative services, preventive and wellness services, and pediatric services.[1]

Hospital and Emergency Care

Hospital stays, surgeries, emergency care, and related treatment are core parts of comprehensive coverage.[1]

Doctor and Outpatient Services

Office visits, specialist care, outpatient treatment, labs, imaging, and follow-up care are typically included.[1]

Prescription and Mental Health Benefits

Comprehensive plans generally include prescription drug coverage and behavioral health treatment.[1]

Preventive Care

Many preventive services are generally covered at no cost when you use an in-network provider.[2]

Another major difference between comprehensive coverage and weaker alternatives is pre-existing-condition protection. Marketplace plans must cover treatment for pre-existing medical conditions, and they cannot reject you, charge you more, or refuse to pay for essential health benefits because of your health history. For a more detailed breakdown, see pre-existing conditions and major medical insurance.[2]

Major Medical vs. Other Coverage Types

One of the biggest mistakes shoppers make is assuming every health-related product works the same way. It does not. Major medical insurance is broad, regulated coverage. Other products may be temporary, limited, or supplemental. That is why you should compare what the product actually does before focusing on brand names alone.[4]

How Plan Types Affect Flexibility

Even when two plans are both major medical, they may work very differently. Marketplace plans come in network structures like HMO, PPO, EPO, and POS. Some mainly steer you toward in-network doctors and hospitals, while others offer more flexibility for out-of-network care at a higher cost.[3]

HMO

Often lower-cost, but usually restricts routine care to the plan’s network except in emergencies.[3]

PPO

Usually offers more provider choice and some out-of-network flexibility, but often at a higher cost.[3]

EPO

Usually keeps care in-network like an HMO, but may differ in referrals and network design.[3]

POS

Blends features of managed care and out-of-network access, depending on the plan’s rules.[3]

How Costs Work in a Major Medical Plan

The monthly premium is only one part of the real cost. You also need to compare the deductible, copays, coinsurance, and the out-of-pocket maximum. In practical terms, the out-of-pocket maximum is the most you pay for covered services in a plan year before the plan pays 100% of covered services for the rest of the year under the plan’s rules.[3]

What to Compare

- Premium: what you pay each month to keep the plan active

- Deductible: what you usually pay before the plan starts paying for many covered services[3]

- Copay: a set dollar amount for certain covered services

- Coinsurance: your percentage share of covered costs after the deductible in many cases[3]

- Out-of-pocket maximum: the annual cap on covered cost-sharing under the plan’s rules[3]

Marketplace plans are also grouped into Bronze, Silver, Gold, and Platinum categories. These metal levels do not measure care quality. They describe how costs are generally split between you and the plan.[3]

If you are comparing brands instead of only plan structure, our guide to top major medical insurance providers is the next step after this page.

How to Choose the Right Major Medical Plan

The best plan is rarely the one with the cheapest premium alone. A better approach is to compare total cost, prescription coverage, provider access, and enrollment timing together. If you are outside Open Enrollment, you may need a qualifying event to unlock a Special Enrollment Period.[3]

Smart Shopping Checklist

- Confirm that your doctors, specialists, hospitals, and pharmacies are in-network

- Check whether your prescriptions are on the plan formulary

- Compare the deductible, coinsurance, and out-of-pocket maximum together

- Think about how often you actually use medical care, not just what you hope to spend

- Review whether an HMO, PPO, EPO, or POS structure fits your preferences[3]

- Make sure you are comparing major medical coverage, not only temporary or supplemental products[4]

Why This Coverage Matters for Health and Financial Stability

Major medical health insurance matters because it combines ongoing access to care with protection against very large medical bills. It supports preventive services, covers treatment for pre-existing conditions, and creates a structure for managing care across doctor visits, prescriptions, emergency services, and hospital treatment.[1] [2] [3]

That does not mean every plan is equal. Some are stronger for low monthly premiums, others are better for regular prescriptions or ongoing specialist care, and some are a better fit only when paired with extra support. The key is to understand what is primary comprehensive coverage and what is simply an add-on.

FAQ

Is major medical health insurance the same as Obamacare?

Not always in casual conversation, but many people use the term when talking about ACA-compliant comprehensive coverage. Marketplace plans under the ACA are major examples of comprehensive major medical insurance.[1]

Does major medical insurance cover pre-existing conditions?

Marketplace plans must cover treatment for pre-existing conditions and cannot charge you more or deny essential health benefit coverage because of your health history.[2]

Is short-term medical the same as major medical?

No. Short-term and fixed-indemnity products are different from comprehensive coverage and should not be treated as automatic substitutes for a full major medical plan.[4]

How do I know which plan type is best?

Start with your doctors, prescriptions, expected usage, and budget. Then compare the network type, metal level, deductible, and out-of-pocket maximum instead of choosing by brand alone.[3]

Need help understanding your options?

Use this page as your foundation, then compare benefits, carriers, and plan types before you enroll.

References

-

HealthCare.gov, What Marketplace health insurance plans cover.

https://www.healthcare.gov/coverage/what-marketplace-plans-cover/

↩ -

HealthCare.gov, Marketplace health plans cover pre-existing conditions and Preventive health services.

https://www.healthcare.gov/coverage/pre-existing-conditions/ |

https://www.healthcare.gov/coverage/preventive-care-benefits/

↩ -

HealthCare.gov, Health plan categories: Bronze, Silver, Gold & Platinum, Health insurance plan & network types: HMOs, PPOs, and more, and Your total costs for health care: Premium, deductible, and out-of-pocket costs.

https://www.healthcare.gov/choose-a-plan/plans-categories/ |

https://www.healthcare.gov/choose-a-plan/plan-types/ |

https://www.healthcare.gov/choose-a-plan/your-total-costs/

↩ -

CMS, Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage.

https://www.cms.gov/newsroom/fact-sheets/short-term-limited-duration-insurance-and-independent-noncoordinated-excepted-benefits-coverage-cms

↩

About the Author

Major Medical Insurance Editorial Team

This article was reviewed and updated using current federal health coverage resources. It is intended for general educational purposes and should not replace official plan documents, Marketplace materials, or licensed advice tailored to your state, eligibility, and medical needs.