By MajorMedicalInsurance.com Editorial Team

Published on April 18, 2026 · Updated on April 18, 2026

Supplemental Health Guide

Supplemental Coverage: What It Is, What It Covers, and When It Makes Sense

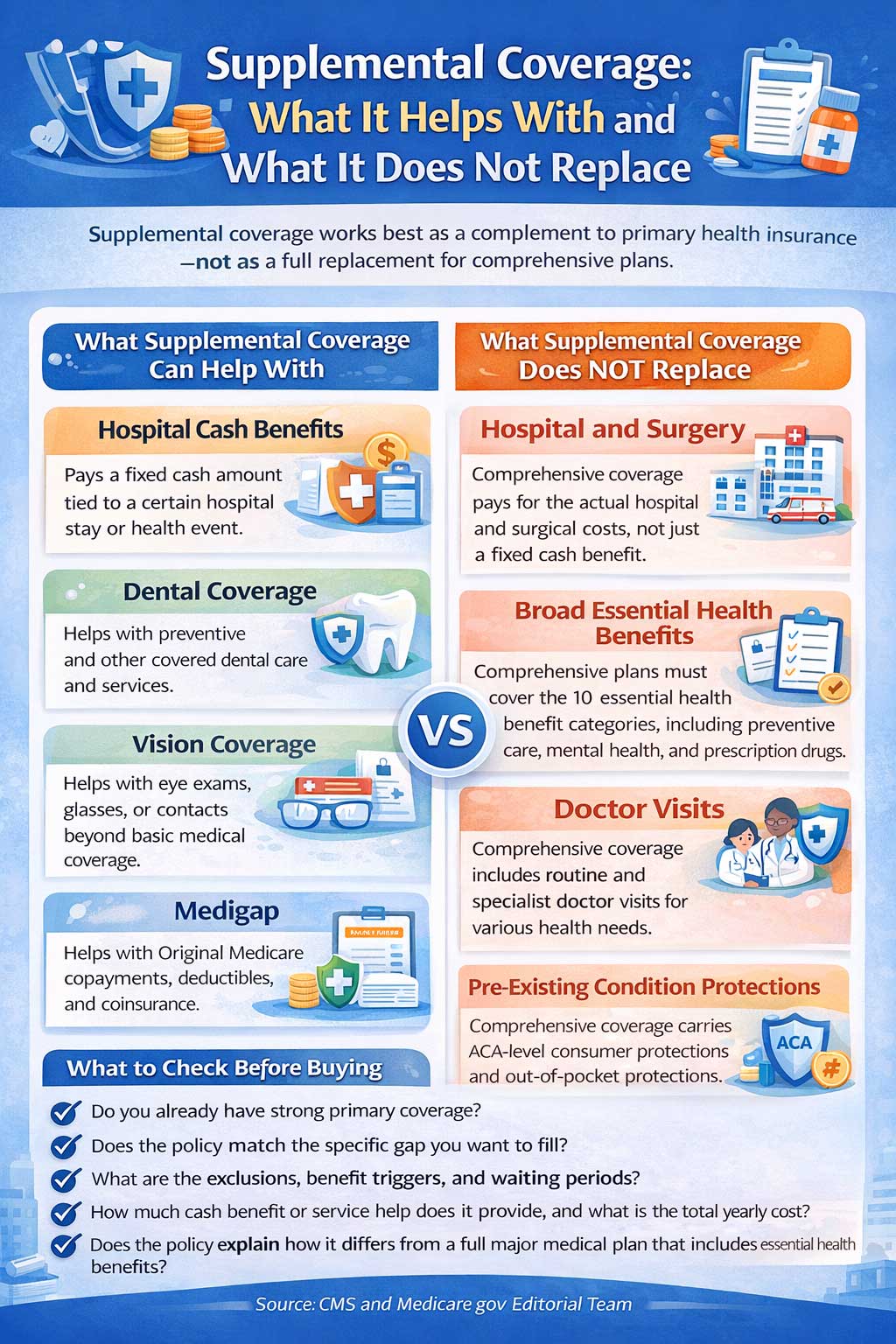

Supplemental coverage is extra insurance meant to add a layer of protection on top of your primary health coverage or, in some cases, to help with specific costs or benefit gaps. Depending on the product, it may pay fixed cash benefits, help with Original Medicare cost-sharing, or add benefits such as dental or vision. It is usually narrower than comprehensive medical insurance and should not be treated as a full replacement for primary coverage.[1][2][8]

What it is

Extra coverage designed to help with specific gaps, extra services, or out-of-pocket costs rather than replace broad medical insurance.[1][2]

What it is not

Many supplemental products are not comprehensive coverage and may not include the federal protections people expect from major medical insurance.[1][8]

What supplemental coverage really means

In practical consumer terms, supplemental coverage means an extra policy layered over your main coverage strategy. It can help in different ways depending on the product. Some policies pay a fixed cash amount when a health-related event happens. Others are designed to cover a narrow category of services, such as dental or vision. Medicare beneficiaries may also use supplemental coverage in the form of Medigap to help pay deductibles, copayments, and coinsurance in Original Medicare.[1][2][4][5]

That does not mean all supplemental products work the same way. Some are true medical complements, while others are limited-benefit or excepted-benefit products. Because of that, a supplemental policy should generally be evaluated as support coverage, not as your only coverage plan. If you still need a primary coverage foundation, start by reviewing broader options such as ACA-compliant coverage instead of trying to build your health protection around a limited supplement.

Common types of supplemental coverage

When supplemental coverage can add value

- You already have primary medical coverage, but want help with certain out-of-pocket exposure or service gaps.[1]

- Your main health plan does not include adult dental or adult vision, and you want dedicated extra coverage for those services.[4][5]

- You are in Original Medicare and want extra protection from deductibles, copayments, and coinsurance through Medigap.[2]

- You want fixed cash benefits that could help with non-medical expenses during a covered health event, such as rent, transportation, or lost income pressure.[1]

When supplemental coverage is often misunderstood

- When people assume it covers the same broad services as major medical insurance.[1][8]

- When shoppers buy a cash-benefit policy thinking it will function like comprehensive hospital and doctor coverage.

- When buyers focus only on premium and ignore exclusions, benefit triggers, waiting periods, and network or claim rules.[9]

- When a person needs real primary health coverage but buys only a narrow supplement or a temporary policy instead.[1]

Supplemental coverage vs. primary medical coverage

The most important distinction is this: supplemental coverage is usually designed to add something to an existing coverage structure, while primary medical coverage is designed to serve as the main engine for hospital, physician, preventive, and other core medical benefits. Most Marketplace plans must cover essential health benefits, and most must also cover certain preventive services at no cost when provided in-network under the plan’s rules.[6][7]

That is why supplemental coverage usually works best when it is layered onto a solid primary plan rather than used as the plan itself. If you are comparing broader coverage against limited protection, our guides on Obama Care / ACA and short-term medical coverage can help clarify the difference.

Important protections and limitations to understand

Another issue people miss is that not every supplemental policy carries the same billing protections as comprehensive health insurance. CMS states that services covered by fixed-indemnity excepted benefits plans, such as hospital indemnity insurance, are not part of the No Surprises Act billing protections. CMS also says those balance-billing protections generally do not apply to vision-only and dental-only insurance plans, although they may apply when vision or dental benefits are included inside a broader health plan.[1][7]

That does not make supplemental coverage useless. It just means you need to match the product to the job. A fixed-indemnity policy can sometimes help as a cash-support layer. A dental policy can help with routine oral care. A Medigap plan can make Original Medicare more predictable. But none of those products should be evaluated as if they all solve the same problem.

How to evaluate a supplemental policy before you buy

- Start by identifying the gap you are trying to solve: hospital cash exposure, dental, vision, Medicare cost-sharing, or something else.

- Check whether you already have primary health coverage that meets your main medical needs.[6]

- Read the benefit trigger carefully. Some supplemental plans pay only when a specific event occurs, not whenever you receive care.[1]

- Review exclusions, waiting periods, separate premiums, and whether adult benefits are limited or optional.[4][5]

- Compare total yearly cost, not just premium. Deductibles, copayments, and coinsurance can materially change value on the primary plan side too.[9]

- If you are Medicare-eligible, make sure you understand whether Medigap or Medicare Advantage is the better fit for your situation, because they do not function the same way.[2][3]

Where this fits on this site

If you are trying to understand whether a supplemental product can stand on its own, read our ACA overview first. If your focus is fixed cash benefits during a hospitalization, compare this page with our guide to hospital indemnity insurance. If you are looking at temporary coverage rather than supplemental coverage, review short-term medical insurance.

For Medicare readers, supplemental coverage often points to Medigap, while Medicare Advantage is a different path for getting Medicare benefits. If you need help choosing which kind of protection to compare next, visit our home page or contact page.

References

- CMS — Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage (Fact Sheet) ↩

- Medicare.gov — Get Medigap Basics ↩

- Medicare.gov — Learn How Medigap Works ↩

- HealthCare.gov — Dental Coverage in the Marketplace ↩

- HealthCare.gov — Vision Coverage Glossary ↩

- HealthCare.gov — What Marketplace Plans Cover ↩

- CMS — Know Your Rights ↩

- CMS — Affordable Care Act Basics (Training Material) ↩

- HealthCare.gov — Your Total Costs for Health Care: Premium, Deductible, and Out-of-Pocket Costs ↩

MajorMedicalInsurance.com Editorial Team

This article was prepared using current CMS, HealthCare.gov, and Medicare materials to explain how supplemental coverage works in the United States, where it may add value, and where it should not be mistaken for full primary medical coverage. It is intended for educational purposes and should be reviewed alongside official plan documents and licensed guidance before enrollment.

Reviewed for clarity, consumer usefulness, and alignment with current public health coverage guidance.