By MajorMedicalInsurance.com Editorial Team

Published on · Updated on

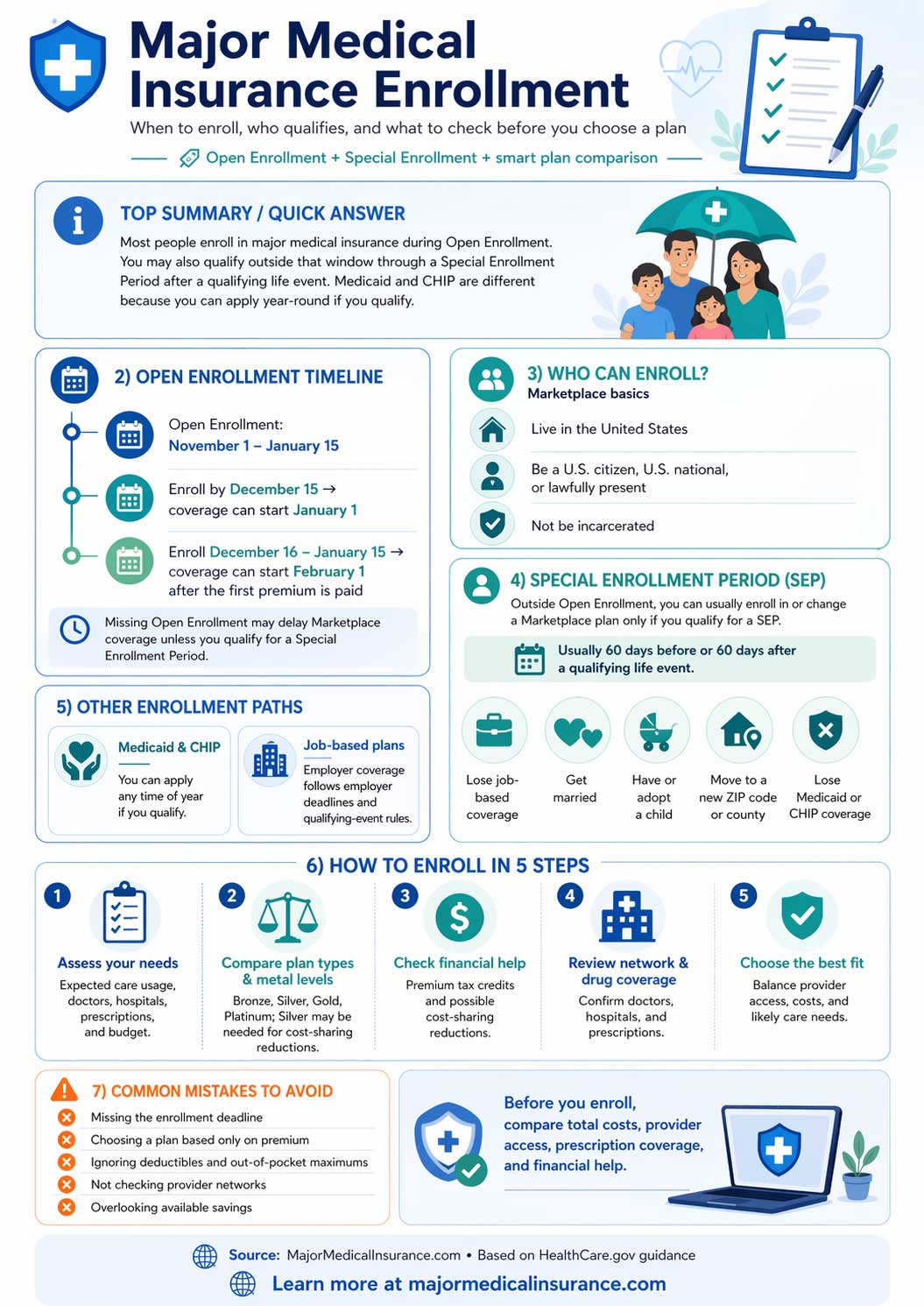

If you need major medical coverage, the main time to enroll in a Marketplace plan is during the annual Open Enrollment Period. On HealthCare.gov, Open Enrollment runs from November 1 through January 15 each year. If you need help applying, you can use HealthCare.gov or call the Marketplace at 1-800-318-2596.[1]

Quick Answer

Most people enroll in major medical insurance during Open Enrollment, but you may also qualify outside that window through a Special Enrollment Period after a qualifying life event. Medicaid and CHIP are different because you can apply for them any time of year if you qualify.[1][2]

Understanding Major Medical Insurance

Major medical insurance is comprehensive coverage designed to help pay for serious medical needs, hospital care, preventive services, prescription drugs, and other essential healthcare expenses. Enrollment matters because even a strong plan only works if you enroll at the right time and choose coverage that actually fits your health needs and budget.

Who Can Enroll in Marketplace Coverage?

HealthCare.gov says that, in general, to enroll in Marketplace coverage you must live in the United States, be a U.S. citizen or national or be lawfully present, and not be incarcerated.[1] If you are trying to sort out where you fit, it also helps to review major medical insurance eligibility before you compare plans.

Open Enrollment Period

The annual Open Enrollment Period is when most people can enroll in, renew, or change a Marketplace health plan. On HealthCare.gov, Open Enrollment starts November 1 and ends January 15. If you enroll by December 15, coverage can start January 1. If you enroll between December 16 and January 15, coverage can start February 1 after the first premium is paid.[1]

Why timing matters

Missing Open Enrollment can delay Marketplace coverage unless you qualify for a Special Enrollment Period. That is why enrollment timing is just as important as plan choice.

Special Enrollment Period

Outside Open Enrollment, you can usually enroll in or change a Marketplace plan only if you qualify for a Special Enrollment Period. HealthCare.gov says SEP timing usually gives you 60 days before or 60 days after the qualifying event, depending on the type of SEP.[2]

Common qualifying life events include losing job-based coverage, getting married, having or adopting a child, moving to a new ZIP code or county, losing Medicaid or CHIP coverage, or certain other household and coverage changes.[2]

Medicaid, CHIP, and Job-Based Enrollment

Medicaid and the Children’s Health Insurance Program are different from Marketplace Open Enrollment. HealthCare.gov says you can apply for Medicaid and CHIP any time of year, and if you qualify, coverage can start without waiting for the yearly Open Enrollment window.[2]

Job-based plans work on their own employer timelines. Marketplace deadlines do not automatically control employer plan enrollment, so employees should always check with their employer or benefits administrator for plan deadlines and qualifying-event rules.[1]

How to Enroll in Major Medical Insurance

Step 1: Assess Your Coverage Needs

Before choosing a plan, look at your expected healthcare usage, preferred doctors and hospitals, prescription drug needs, and how much you can realistically handle in premiums, deductibles, and out-of-pocket costs.

Step 2: Compare Plan Types and Categories

When reviewing major medical insurance plans, compare both network structure and metal category. Bronze plans usually have lower premiums and higher out-of-pocket costs. Silver plans usually sit in the middle. Gold and Platinum generally have higher premiums and lower out-of-pocket costs. HealthCare.gov also explains that if you qualify for extra savings called cost-sharing reductions, you must choose a Silver plan to use them.[3]

Step 3: Check Financial Help

Many people qualify for premium tax credits that reduce monthly premium costs. Some also qualify for cost-sharing reductions that lower deductibles, copayments, and coinsurance. If you are comparing individual coverage, our Obamacare / ACA page can help you understand how these Marketplace savings fit into the bigger picture.[3]

Step 4: Review Network and Drug Coverage

Before enrolling, make sure your doctors, hospitals, and prescriptions are handled the way you expect. A lower-premium plan can still become expensive if your providers are out of network or your medications fall into costly tiers.[4]

Step 5: Finalize the Best Fit

If you are buying your own policy, compare your options carefully and choose the plan that matches your likely care needs, provider access, and budget. For more on shopping this market, see major medical insurance for individuals.

Common Enrollment Mistakes to Avoid

- Missing the enrollment deadline and creating a coverage gap

- Choosing a plan based only on premium

- Ignoring deductibles and out-of-pocket maximums

- Failing to check whether your doctors and hospitals are in-network

- Overlooking available premium tax credits or Silver-plan extra savings

Bottom Line

Major medical insurance enrollment is not just about signing up for any plan before the deadline. It is about enrolling at the right time, understanding whether you qualify for Open Enrollment or a Special Enrollment Period, checking whether Medicaid or CHIP might apply, and comparing plan categories, provider networks, and financial help carefully. A little attention at enrollment can make a big difference in both coverage quality and total cost.

References

-

HealthCare.gov, Tips about the Health Insurance Marketplace®, Are you eligible to use the Marketplace?, and When can you get health insurance?.

https://www.healthcare.gov/quick-guide/one-page-guide-to-the-marketplace/ |

https://www.healthcare.gov/quick-guide/eligibility/ |

https://www.healthcare.gov/quick-guide/dates-and-deadlines/

↩ -

HealthCare.gov, Special Enrollment Period and Medicaid & CHIP coverage.

https://www.healthcare.gov/coverage-outside-open-enrollment/special-enrollment-period/ |

https://www.healthcare.gov/medicaid-chip/

↩ -

HealthCare.gov, How to Save Money on Monthly Health Insurance Premiums, Cost-sharing reductions, and Health plan categories: Bronze, Silver, Gold & Platinum.

https://www.healthcare.gov/lower-costs/save-on-monthly-premiums/ |

https://www.healthcare.gov/lower-costs/save-on-out-of-pocket-costs/ |

https://www.healthcare.gov/choose-a-plan/plans-categories/

↩ -

HealthCare.gov, 3 things to know before you pick a health insurance plan.

https://www.healthcare.gov/choose-a-plan/comparing-plans/

↩